At any given point in time, the housing market predictions for next 5 years are based on various macroeconomic factors interplaying with one another. GDP shifts, vacancy rates, regional variations, and policy changes all play a role in shaping the real estate market through 2030 and beyond.

At Defy Mortgage, we provide comprehensive lending solutions designed to simplify the mortgage process. Whether you’re a self-employed individual seeking an affordable home loan, a business owner looking to expand your investment portfolio, or a homeowner interested in tapping into your stored home equity, we have the expertise to help you realize your goals.

As your trusted mortgage partner, we closely monitor expert predictions for the U.S. housing market. Although we can’t offer you financial advice, we can help you better understand the economic trends defining the real estate landscape in the next five years. In this guide, we’ll discuss various expert forecasts and developments that are anticipated to impact the real estate market. We’ll also go over what this all means for real estate investors.

Let’s jump in.

Economic and Housing Market Trends Shaping 2025-2030

Housing market predictions for next 5 years mostly agree that price growth is headed for an eventual slowdown, although prices are still expected to increase through 2030.

Since mortgage rates generally tend to move with the Fed rate, they hit fourth-month lows at the time of writing (March 2025). When the 10-year Treasury Note’s yield goes down, 30-year mortgage rates often follow, which helps make it cheaper to borrow money. This will likely cause ripple effects throughout the housing market.

Some experts anticipate mortgage rate decreases alongside potential Fed rate cuts in 2025 and beyond, but keep in mind that mortgage rates are impacted by many other market factors as well.

Price Growth Slowdown or Correction?

Is the housing market going to crash? Most analysts anticipate that home prices will gradually stabilize, although some warn that the market could be headed toward a correction, with many local markets significantly overvalued.

For example, some experts voiced concerns about price correction in areas like Miami and Orlando where homes are almost 40% overvalued in 2024. Orlando saw an overall sales drop of around 7% in 2024, and while Miami’s sales rose by 3% overall in 2024, it was also one of five markets (all in Florida) where sales fell faster than any other market in the US year over year for a four-week period ending on November 10, 2024. During this period, sales dropped by 14%.

Regional Variations

Changing migration trends are one of the primary factors that lead to changes in demand. For example, Miami and Orlando, considered by experts to be ripe for market correction, were also migration hotspots during the massive domestic migration wave that occurred between 2020 and 2023. The influx of new residents rapidly drove up housing demand and prices. Conversely, people moving away from places like San Francisco has led to a consistent drop in property value in recent years.

San Francisco is also a prime example where other local economic factors contributed to changes in demand. While it may still be one of the priciest places to live, single-family homes in San Francisco have now fallen roughly 15% from their 2022 peak. Many publications reported that the downturn aligns with the tech industry from the local job market.

Insurance and its Housing Market Effects

As traditional housing affordability gradually improves, the rapidly increasing cost and decreasing availability of homeowners’ insurance are creating a new barrier to homeownership and housing stability. Even if mortgage rates soften and home prices normalize in the next five years, the market can face additional pressure from the ongoing homeowners’ insurance crisis.

In recent years, insurance companies have dropped hundreds of policies, citing higher risks often due to climate-related crises. Regulatory changes will be in play in the next five years and they can directly impact how the housing market performs in disaster-prone areas.

General Economic Trends

Lawrence Yun, chief economist of the National Association of Realtors, predicts that home buyers will enjoy a lower mortgage rate of around 6% in 2025 after it has averaged around 7% for the past few years.

For many homebuyers, an interest rate drop of even 1% can be a great opportunity to purchase their first home or finally acquire interested buyers for their property. Here are the notable economic variables that are contributing to this outlook :

- Treasury to Temper Bond Yield Growth: One of the primary drivers of mortgage rates is the 10-year Treasury Bond yield, which mortgage bonds must compete with in terms of profitability. Treasury Secretary Scott Bessent has expressed a commitment to keep the yield below the 5% threshold. With a lower Treasury Bond yield, mortgage bonds have a lower target to compete with, encouraging lenders to lower rates to maximize affordability.

- Rising Buyer Interest: Recent data shows that default rates are down, while housing demand is up for both Millennials and Gen Z buyers, which could signal stable demand from these cohorts in the future.

- Inflation Trends: The Consumer Price Index was reported to have increased 0.5% between December 2024 and January 2025, and 3.0% over the past 12 months. Core inflation, which excludes volatile commodities such as food and energy, experienced a 12-month percentage change of 3.3% as of January 2025, although this rate has been on the decline since 2022.

- Stable Job Market: The United States added 143,000 jobs in January 2025, which was lower than economists predicted. However, the unemployment rate decreased from 4.1% to 4.0%, ahead of forecasts.

- Wage Growth: The continued growth of wages and GDP is also adding to buyer purchasing power, especially in areas such as the Miami metro area, which has experienced a 41.7% increase in wages since 2015. Across the US, wages and salaries increased 4.5% between December 2023 and December 2024.

With price growth slowing down, wage growth could eventually outrun rising prices and make homeownership more affordable.

Recent Mortgage Rate Drops

Signs of mortgage rates falling are already manifesting. As of March 2025, the average rate for the 30-year fixed rate mortgage has fallen to 6.69%, the lowest it’s been in 4 months. 15-year fixed mortgages, on the other hand, have fallen to 6% on average.

This signals an incredible opportunity for homebuyers and homeowners to lock in favorable rates. Additionally, the mortgage market with new buyers adds significant liquidity to lenders, potentially driving down rates even further.

Policy Changes

Government policies can have far-reaching effects on the economic trajectory of a nation. Here are some of the most impactful policy changes that experts speculate will have a significant effect on the housing market:

- The Privatization of Fannie Mae and Freddie Mac: Scott Turner, the new secretary for the Department of Housing and Urban Development (HUD), announced that Fannie Mae and Freddie Mac are slated to become fully private in a bid to make housing more affordable and accessible. However, removing government backing could harm investor confidence, leading to higher mortgage rates as lenders try to counterbalance the added risk.

- Interest Rate Policies: The recent positive outlook on mortgage rates was influenced by the Federal Reserve cutting rates last year. While the Fed’s rate cuts do not directly correlate to lower mortgage interest rates, they can indirectly impact them by influencing other aspects of the economy, such as consumer spending and overall economic growth. Lower Fed rates stimulate demand and often reduce borrowing costs.

- Zoning Reforms: Because one of the most effective ways of driving down prices is to create more supply, initiatives such as the Housing Supply Action Plan have been making homes more affordable in disadvantaged communities by removing zoning ordinances. The Center for American Progress is also putting forward a proposal that aims to reform local land use across the US, which could have a sweeping effect over the next five years if approved.

Downsizing Homes

Recent data released by the National Association of Home Builders (NAHB) reveals a notable downward trend in U.S. residential construction. The median size of newly built American homes decreased from 2,200 square feet in 2023 to 2,150 square feet in 2024, marking the smallest median home size recorded in the past 15 years. Even at 2150 square feet, a typical American home is still twice the average size of a home in Japan, for example.

For decades, American homes have trended larger. This decrease represents a significant shift in the housing market, reflecting changing economic conditions, rising construction costs, and evolving consumer preferences. The availability of smaller homes can potentially lower the total cost of the home, enabling more potential buyers to secure their first home.

Implications for Real Estate Investors in 2025-2030

So, what does all of the above mean for real estate investors? With the consensus being that prices will continue to rise, undervalued markets will likely appreciate, giving investors who want to flip houses or buy and rent an easy foot in the door. While we can’t give financial advice, here are some potential implications of these trends and how they may impact the next five years:

Capitalizing on Emerging Markets

Identifying undervalued regions is essential if you’re interested in capitalizing on continued growth. Price growth remains positive in key markets where housing demand continues to outpace supply. Look at regions that are undergoing zoning reforms, infrastructure investments, population shifts, and other factors that are likely to create sustained price appreciation.

Areas undergoing rapid appreciation are particularly suited to short-term financing options such as fix-and-flip loans and construction loans. These loans allow you to begin construction or renovations just before prices in an area are expected to rise.

Rental Market Shifts

The rental sector could see increased demand in areas where homeownership becomes less affordable due to continually rising prices. Areas with consistent population growth and limited housing inventory, such as Dallas, Orlando, and Honolulu, are particularly suited for this.

In markets like these, investors might find opportunities in multifamily housing developments to fill the gap left by lack of homeownership, as prices have yet to correct. Honolulu in particular is currently undergoing significant land reforms that are opening up fresh opportunities in new mixed-use areas. This is the perfect environment to tap into with a DSCR loan. Other parts of Hawaii, such as Maui, are quickly following suit, broadening the landscape in an already robust rental market.

Prepare for Economic Volatility

New policies could unexpectedly disrupt the housing market’s current trajectory. To hedge against economic fluctuation and the potential tightening of financing options, consider non-QM loan products such as debt service coverage ratio (DSCR) loans. These alternatives may provide greater flexibility in uncertain economic times.

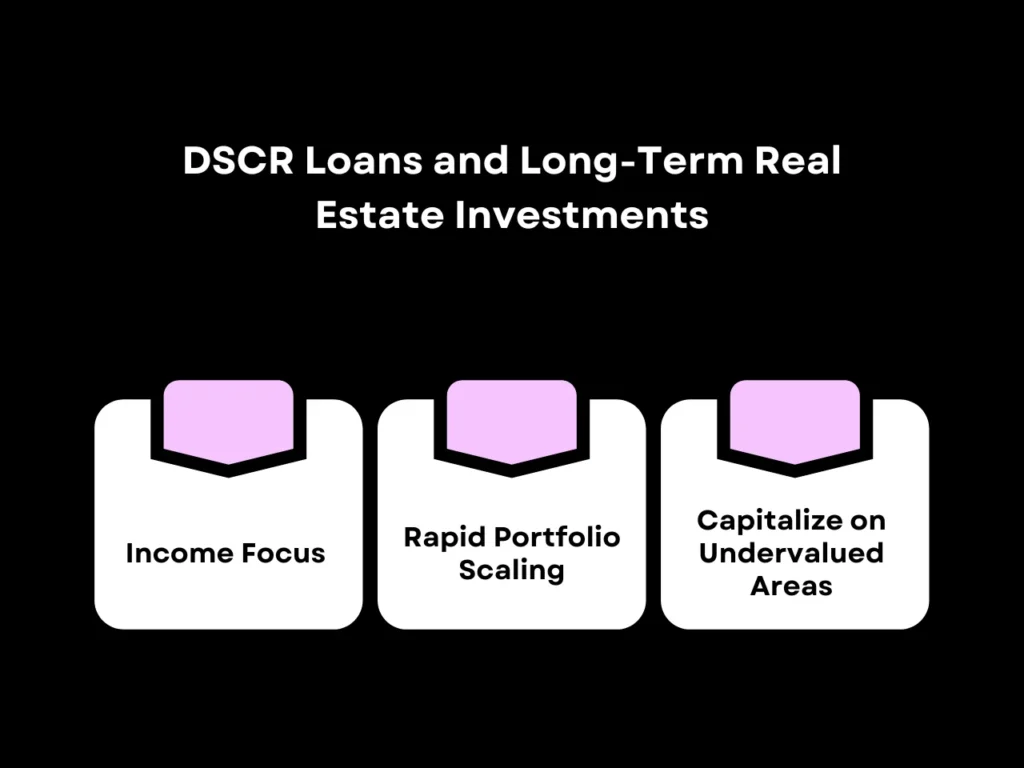

DSCR Loans and Long-Term Real Estate Investments

A DSCR loan is a mortgage option that bases terms such as rates and loan amounts on the property’s potential to generate income instead of the investor’s financial profile. This makes it well-suited for long-term real estate investments. Let’s look into why:

- Income Focus: DSCR loans are primarily concerned with how much rental income a property can generate at full capacity. This means that even with lower credit scores or higher debt-to-income (DTI) ratios, you can secure an affordable DSCR loan for a lucrative investment property and start earning returns.

- Rapid Portfolio Scaling: There’s no limit to how many active DSCR loans you can have at a time, as long as lenders are willing to approve you. This enables you to quickly grow a portfolio and scale your rental income.

- Capitalize on Undervalued Areas: Having a collection of lucrative, well-maintained properties in an area poised for growth sets you up for even bigger long-term gains should you decide to sell in the future.

With market uncertainties on the horizon, a stable, long-term investment can be invaluable. DSCR loans are one of the best ways to secure that.

Housing Market Predictions For Next 5 Years FAQ

What factors are expected to drive housing market trends in the next five years?

Economic conditions such as interest rate changes, population growth, and wage shifts define the current housing market landscape. Housing supply and policy changes can also impact the housing market in the US.

Will housing prices increase or decrease by 2030?

The general consensus is that prices will continue to increase but at a slower rate. However, some experts caution that corrections may be in store, particularly in overvalued markets in specific regions.

How will regional differences impact housing market growth?

Regional differences that can affect the housing market include: which areas will be first to implement zoning policy changes, domestic migration shifts, growing job markets, and infrastructure developments. Some regions will be more susceptible to factors that cause home value to appreciate, such as new arrivals who drive up demand in particular sectors of the housing market, such as exurban locations.

Is it a good idea to invest in rental properties over the next five years?

Rental properties in high-growth areas with strong demand, such as Honolulu, are likely to remain a solid investment. However, it’s worth noting that diversifying your portfolio with properties that generate a positive cash flow can insulate you from market shocks such as price corrections, giving you an incentive not to rely solely on appreciation.

How do DSCR loans benefit long-term real estate investors?

DSCR loans allow investors to secure financing based on a property’s income rather than personal financial history, making it easier to expand rental portfolios and navigate market fluctuations.

What are the biggest risks for housing market investors in this timeframe?

Sudden market corrections, regulatory changes, and shifts in demand patterns could disrupt expected growth trajectories and thus investors’ strategies. This can be mitigated by diversifying your investments and focusing on strong fundamentals such as market resilience and favorable locations.

Key Takeaway

While the housing market predictions for next 5 years primarily involve continued yet decelerating price growth, regional fluctuations can cause significant corrections in several major markets. However, the housing market will be increasingly shaped by a complex interplay of factors.

As the median price of homes continues to increase over the remainder of the decade, opportunities still exist for those looking to capitalize on rising markets. Investors will need to diversify geographically and stay informed in order to hedge against volatility.

Need help rethinking your financial strategy going into 2025 and beyond? Defy offers a free consultation. Simply schedule an appointment on our website, call us at (615) 622-1032, or email us at team@defymortgage.com. Let’s build your winning strategy together.